핵심 요약

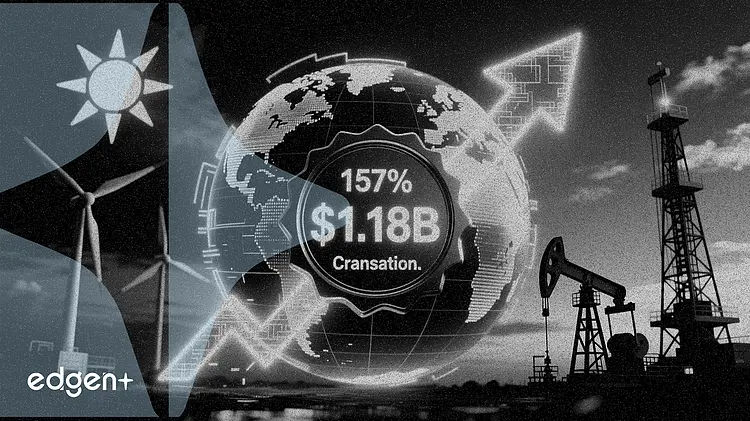

- 2026년 1분기 조정 잉여현금흐름이 전년 동기 대비 157% 성장한 1억 6,000만 달러를 기록했다고 발표했습니다.

- 파트너사인 칼라일 그룹과 함께 오클라호마의 카미노 내추럴 리소스 자산을 11억 7,500만 달러에 공동 인수한다고 발표했습니다.

- 이번 거래로 하루 약 51,000배럴의 석유 환산 생산량이 추가되며, 혁신적인 증권화 구조를 통해 자금을 조달합니다.

핵심 요약

다이버시파이드 에너지(Diversified Energy Co.)는 1분기 조정 잉여현금흐름이 전년 대비 157% 급증했다고 보고하는 동시에, 투자 회사인 칼라일(Carlyle)과 함께 오클라호마 아나다코 분지의 자산을 11억 7,500만 달러에 공동 인수한다고 발표했습니다. 이는 이 생산 기업에 있어 새로운 확장 단계와 참신한 자금 조달 전략을 시사합니다.

다이버시파이드의 CEO인 러스티 헛슨 주니어(Rusty Hutson, Jr.)는 "최근 완료된 셰리던(Sheridan) 인수와 파트너사인 칼라일 그룹과 함께 3분기에 완료될 예정인 혁신적 구조의 카미노(Camino) 인수를 통해 우리는 다시 한번 플랫폼을 변화시키고 있습니다"라고 말했습니다. "우리의 규모는 발전, 데이터 센터 성장, LNG 수출, 그리고 미국 에너지 생산의 지속적인 중요성을 포함한 강력한 장기 수요 동력으로부터 다이버시파이드가 혜택을 입을 수 있는 위치에 있게 합니다."

3월 31일 종료된 3개월간의 강력한 실적을 보면 조정 EBITDA는 전년 동기 대비 108% 증가한 2억 8,700만 달러를 기록했으며, 조정 잉여현금흐름은 1억 6,000만 달러에 달했습니다. 이러한 성과는 1억 6,100만 달러의 순손실 보고에도 불구하고 이루어졌는데, 회사 측은 해당 분기 동안의 상당한 원자재 가격 변동성으로 인한 미결제 파생상품에 대한 3억 9,800만 달러의 비현금성 손실이 포함된 결과라고 설명했습니다. 일평균 생산량은 11억 9,800만 입방피트 환산량(MMcfepd)이었습니다.

카미노 내추럴 리소스(Camino Natural Resources)로부터 자산을 인수하기 위한 칼라일과의 거래는 주요 미국 에너지 분지 내 다이버시파이드의 입지를 확장하는 중요한 전략적 행보를 나타냅니다. 이번 거래 구조를 통해 다이버시파이드는 자산을 운영하고 미개발 지역을 보유하는 동시에, 맞춤형 자산유동화증권(ABS)을 사용하여 생산 자산을 조달할 수 있게 되는데, 이는 향후 대규모 인수를 위한 길을 열어줄 수 있는 모델입니다. 이 거래는 2026년 3분기에 마감될 예정입니다.

다이버시파이드의 1분기 실적은 상당한 현금 흐름을 창출하는 능력을 강조했습니다. 회사는 배당금과 자사주 매입을 통해 주주들에게 9,400만 달러를 환원했으며 9,200만 달러의 부채를 상환하여 재무 상태를 강화했습니다. 레버리지 비율은 3월 31일 기준 2.2배로, 목표 범위인 2.0배에서 2.5배 이내를 유지했습니다.

생산량은 천연가스 약 71%, 천연가스 액체(NGL) 14%, 원유 15%로 구성되었습니다. 회사는 단위당 지표가 매버릭 내추럴 리소스와 캔버스 에너지의 2025년 인수를 통해 액체 비중이 높은 자산이 통합된 점을 반영하고 있으며, 시간이 지남에 따라 비용 시너지 효과가 실현될 것으로 기대된다고 언급했습니다.

카미노 인수는 생산 자산을 보유하고 ABS 부채를 발행할 새로운 특수목적법인(SPV)을 통해 구성됩니다. 칼라일이 이 SPV의 과반수 지분을 보유하며, 다이버시파이드는 자산 운영자 및 관리자 역할을 수행하게 됩니다. 결정적으로, 다이버시파이드는 SPV 외부에서 100개 이상의 확인된 시추 준비 위치를 포함한 미개발 자산에 대한 완전한 소유권을 유지하게 됩니다.

이러한 혁신적인 구조를 통해 다이버시파이드는 운영 규모를 확장하고, 기존 신용 한도를 통해 조달한 약 2억 1,000만 달러의 순지출로 약 3억 입방피트 환산량의 생산량을 추가할 수 있습니다. 이번 거래는 다이버시파이드의 기존 오클라호마 포트폴리오와 인접한 자산을 추가함으로써 운영 효율성으로 가는 즉각적인 경로를 제공합니다.

회사는 2026년 전체 가이던스를 재확인했으며, 조정 EBITDA는 9억 2,500만 달러에서 9억 7,500만 달러 사이, 조정 잉여현금흐름은 약 4억 3,000만 달러로 전망했습니다. 이 가이던스에는 최근 완료된 셰리던 인수나 진행 중인 카미노 거래의 영향이 아직 포함되지 않아, 향후 상향 조정될 가능성을 시사합니다. 헛슨 CEO는 회사의 확장된 입지와 입증된 비즈니스 모델이 장기적인 에너지 수요 트렌드를 활용하고 주주 가치를 높일 수 있는 위치에 있다고 자신감을 표했습니다.

이 기사는 정보 제공 목적으로만 작성되었으며 투자 조언을 구성하지 않습니다.