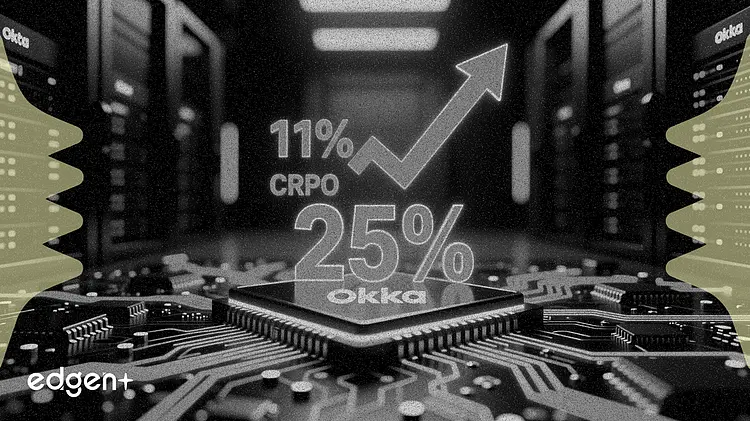

Okta reported new product bookings reached 25% of total in Q1, as AI agent pipeline emerged as the fastest-growing identity segment.

"AI agents are the fastest-growing identity in the enterprise, but also the least governed," Chief Executive Officer Todd McKinnon said on the earnings call.

The company guided Q2 current remaining performance obligations growth of 11% and full-year revenue growth of 9% to 10%. New products, led by Okta Identity Governance, drove a 40% annual contract value uplift when included in deals, McKinnon said. Large customers now represent 85% of annual contract value, up from 80% previously.

Shares rose 1.7% to $93.81. The results come as Okta prepares to manage AI agents as "first-class identities," with management calling agentic AI a fiscal 2028-2029 opportunity.

AI Pipeline and Partner Momentum

Okta for AI Agents reached general availability in April. Chief Financial Officer Brett Tighe said early AI-specific deals are "significantly larger" than the company's average deal size, while McKinnon described the AI pipeline as "bigger than anything we've ever seen." He cautioned that converting that pipeline into revenue remains the challenge.

Partner-sourced bookings increased meaningfully in the quarter and included multiple deals worth more than $1 million, Tighe said. The company shifted more professional services work to global systems integrators to increase scale.

Okta ended the quarter with approximately $2.6 billion in cash and short-term investments. The company repurchased 3 million shares for $241 million during Q1, with $680 million remaining under its $1 billion buyback program. Okta plans to settle the remaining $350 million in convertible notes in cash next month.

The AI opportunity raises Okta's strategic importance with enterprise customers, McKinnon said, driving broader interest in governance, privileged access and identity infrastructure. Cantor Fitzgerald raised its price target to $110 from $100, maintaining an Overweight rating, citing workforce identity as the dominant growth driver. Guggenheim reiterated a Buy rating with a $138 target, while Barclays upgraded the stock to Overweight. The firm's channel checks flagged competitive pressure from Microsoft in platform depth outside core identity and access management. Investors will watch the Q2 earnings call for signs of AI pipeline conversion.

This article is for informational purposes only and does not constitute investment advice.